Introduction:

Mark down April 20, 2020 in the energy history books: the first time ever both Western Canadian Select (WCS) and West Texas Intermediate (WTI) traded at negative prices. Yes, you read that right. Traders were being paid to take oil.

The economic impact of COVID-19 has significantly disrupted global economies, particularly the oil and gas industry. Gas stations are in no rush to re-stock inventory with citizens under lockdown. Factories remain shut down or are running at limited capacity. According to BBC, the number of passenger planes have been reduced by 95 per cent. Major US refiners including Marathon Petroleum, Valero Energy and Phillips 66 have lowered and shut down facilities with a lack of fuel buyers. In other words, demand has decreased significantly. Global crude production has been increasing over the past decades to meet growing demand. However, the sudden decrease in demand today has led to an oil market imbalance situation no one expected just a few months back.

This article investigates the fundamentals behind negative oil prices: supply and demand, and as a result, the oil storage shortage.

60 Second Recap:

We highlight some key events impacting global energy markets within the past two months in the timeline below:

WTI Future Contracts

Sourced from FactSet, CNBC Data

Why are Prices Negative?

““When producing oil, you have two options – you either use it or you store it”.”

This brings us back to ECON 101: supply and demand. In the case of oil, production and consumption.

The chart illustrates how production is outpacing consumption levels in Canada over the past decade or so, prior to COVID-19. The impact of the pandemic has further depressed consumption levels. Note that oil imports are not factored in the chart above.

A. Supply / Production

Despite the lack of oil demand, oil producing nations continue to produce, albeit at slightly lower volumes. This has resulted in crude inventories worldwide filling up at an alarming rate. According to the IEA on April 7, global production was 101 million bbl/d in 2019. The production cuts agreed upon in mid-April by OPEC+ and G20 nations will see a 10 million bbl/d reduction from May 1 onwards. Of the cuts, the US, Canada and Brazil are expected to reduce production by 3.7 million bbl/d proportionately.

In Canada, the 2019 average crude production was 4.2 million bbl/d (Statistics Canada). Based on 2019 oil production proportions, Canada is estimated to reduce production by 0.8 million barrels from May onwards, a 16 per cent decline compared to 2019’s average production levels.

We now look at the current situation from the perspective of demand.

B. Demand / Consumption

As most of the world’s population is currently in lockdown, global oil demand has cratered to rock bottom levels. According to the International Energy Agency (IEA), the world consumed an average of 100 million bbl/d in 2019. Of this, Canada consumed 2.5 million bbl/d. Currently, the IEA predicts consumption to have declined by 29 per cent. This is supported by other industry estimates of a 30 per cent decline as per commodity traders Trafigura and Vitol.

By using a 30 per cent reduction assumption in oil consumption today for both Canada and the world, we compare this to oil consumption levels between 1980 and 2018 below:

Data sourced from: BP Statistical Review of World Energy

Based on this analysis, the current global consumption estimate of 70 million bbl/d is similar to the consumption levels 18 years ago in 2002. This was back when Jean Chrétien was Prime Minister, the world was introduced to its first ever cell phone with a built-in camera and Elon Musk had yet to acquire Tesla Motors.

In Canada, the estimated current oil consumption estimate of 1.76 million bbl/d is similar to consumption levels 33 years ago back in 1987. This was back when the Loonie was first introduced, the Canada-US Free Trade Agreement (predecessor to NAFTA) was signed, the first Canadian Starbucks was opened in Vancouver and the Simpsons cartoon first appeared.

A 30 million bbl/d decrease in global consumption is significant. However, the 10 million bbl/d production cut agreed by OPEC+ and G20 nations in mid-April represents only one-third of the consumption decline. We now look at how both oil supply and demand have affected oil inventory storage.

““If your bathtub is about to overflow and you turn down

the tap a little, it will still overflow.” ”

C. Global Storage

Both supply and demand have resulted in oil inventories surging in recent weeks. The EIA’s April 7 forecast estimates global inventories to increase from 5.7 million bbl/d in Q1 to 11.4 million bbl/d in Q2. Inventory levels are projected to be at its highest levels in Q2 before decreasing in the second half of 2020 with the gradual return of economic activity.

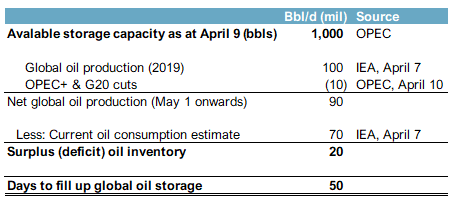

We investigate the number of days before global storage is filled up below:

Based on our analysis, it would take 50 days or until the end of May 2020 for global oil storage to be maxed out under the current conditions.

““1.3 billion barrels will be added to global markets in Q2, exceeding the 1 billion barrel storage capacity available currently by May 2020”. ”

Canadian Crude Storage

According to Oil Sands Magazine (OSM) as of April 14, Canada’s total storage capacity is 96 million barrels with another 7.2 million barrels of storage capacity under construction.

Most Canadian crude storage facilities are located in Alberta, especially in Edmonton and Hardisty. Various predictions on Canadian storage levels are highlighted below:

Source: Oil Sands Magazine, April 17, 2020

Rystad Energy predicted in mid-March that Canadian storage availability would run out by the end of March. The pressure was somewhat eased with producers cutting back on production.

In mid-March, HIS Markit estimated total oil storage in Alberta at between 80 and 85 million barrels, of which 65 - 75 million barrels were currently in storage.

Goldman Sachs predicted on April 1 that commercial inventory levels could be breached within 2-3 weeks if Canadian production is not reduced further.

If the situation persists, producers may face no option but to shut down production. This represents unchartered territory for Canadian producers, where shut down considerations are motivated by both storage limitations the pricing environment However, shutting down Canadian oilsands production incurs the risk of causing permanent damage to the reservoirs, jeopardizing billions of dollars of assets.

South of the Border

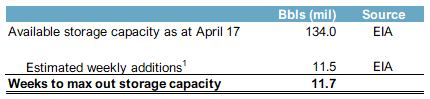

The bulk of Canadian crude is exported south to US refineries. However, the EIA reports that US refinery utilization rates are currently at 68 per cent of total capacity, the lowest since 2008 and just slightly above all-time lows. US storage is filling up fast as well. The EIA also reported on April 17 that total US crude storage capacity was 653 million barrels, with 79 per cent capacity currently utilized.

We investigate the number of weeks before US inventory will be maxed out:

Note:

1. EIA estimates 11.5 million bbls per week in excess supply from April 17 onwards.

Based on this analysis, US storage will be maxed out at the beginning of June, at the latest. Our estimate is supported by the following predictions for comparison:

Goldman Sachs reported on April 17 that Cushing storage will be “stock out” by the first week of May.

IHS Markit’s Oil Price Information Service estimated on April 21 that Cushing storage will be “stock out in two or three weeks” (mid-May).

New York based investment bank Mizuho Securities USA predicted on April 21 that US storage would “fill in 7 to 8 weeks” (mid-June) based on the current increase rate.

““Never before has the oil industry come this close to testing its

logistics capacity to the limit.” ”

When land storage is maximized, the next consideration is storage on sea. Parties considering tanker storage allow tankers to float aimlessly pending a buyer or higher prices. Reuters reported that global oil tankers are hitting maximum capacity as well, with tankage storage rates increasing substantially since January 2020.

“Did you know?

The going daily rate for the largest oil tankers in the world hit

US $180,000 on April 20. ”

Conclusion:

The continuous flood of crude into global markets has created an oil storage crisis the world has never experienced before. The world is staring at 20 million bbl/d of excess product and nowhere to store this by the end of May or the beginning of June. Something must give way and that is the price of oil. Do not be surprised if the price of future contracts becomes negative again in the upcoming months. Tough times ahead.