(but outlook still not great for Oilfield Services)

As North America looks to reopen over the coming weeks, we expect a modest recovery in oil demand. While there will be hiccups along the way during the gradual reopening, an improvement in demand for oil is critical especially for oil producing provinces like Alberta and Saskatchewan. The global energy industry like many, is experiencing a demand shock. This shock will be offset by two concurrent moves: a decrease in supply and a rebound (of some sort) in demand. This article investigates US oil production that has contributed to the surge in supply in recent years, and the recent reduction in production in five key regions.

The supply side, and major driver of the unfortunate oil price war, has been driven by US production increases. The increases are predominantly from a handful of basins: Anadarko, Bakken, Eagle Ford, Niobrara and the Permian. June production numbers are from the May 18th, 2020 EIA Drilling Productivity Report.

*peak production for all five regions combined.

Collectively, these five basins accounted for over 7.4 million bbl/d of production increases over the last decade to the November 2019 peak. Astonishing and a clear indicator of why the Saudis felt a price war was necessary – albeit terrible timing for everyone.

The key driver behind the surge in production is the significant technological improvements, resulting in substantial gains in US production output per rig. Through technology, these regions have seen significant increases in the average new well production per rig[1].

With increased growth in production, we are also seeing significant legacy well production declines month over month. Translation: In order to maintain production levels, many new wells need to come online each month.

For aggregate production to hold or grow, continued improvements in technology to increase existing production are necessary, as well as continued new drilling activity. Over time we are seeing the volumes of legacy production declines increasing, including a large downward ‘blip’ in May 2020. We believe the declining storage capacity and the shut-in of some legacy wells due to the current low price environment contributed to this result, but the long-term trend remains the same: more production is coming offstream from legacy wells, meaning it needs to be replaced to maintain overall production levels.Overall production has been in decline in these basins since late 2019, with June production expected to see an overall decline by over 1.3 million bbl/d.

Decrease in Production From Late 2019 Regional Peak Level

Sourced from U.S. Energy Information Administration

With drilling activity and overall production declining in all these regions even before COVID-19 and the global oil price war, a downward trend in US production was already underway. Since the November 2019 peak of output across these five major regions, we’ve seen a 1.24 million bbl/d decrease in production. According to the EIA’s May 2020 month-over-month drilling productivity report, the most recent monthly decline was 196,000 bbl/d, led by an 87,000 bbl/d decline in the Permian.

Near-Term Outlook: Lower production, soft OFS activity & stronger WTI Prices

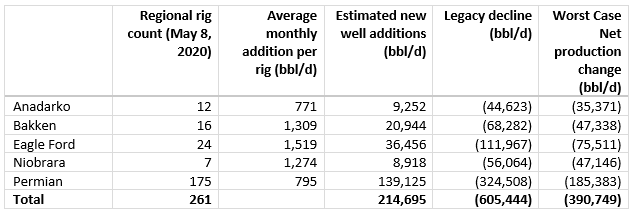

Based on new oil production per rig and legacy production declines, the number of rigs necessary to maintain current production levels is much higher than the current rig counts in each region. We expect to see continued large production declines over the upcoming months, especially in the Permian and Eagle Ford basins. The table below (which represents a worst case scenario) outlines a large bbl/d production decline projection on a monthly basis. Net production is unlikely to reverse until drilling activity begins to rebound, which we don’t expect until 2021 at the earliest.

Potential Net Production Decline Rates at Current Activity Levels

WTI prices should see strength and a bounce back (which is already underway as WTI climbs above $30 per barrel). The next few months should see an additional 1-1.5 million barrels/day of additional net declines in US production from these basins as producers scale back spending, conserve cash, and preserve balance sheets. Additionally, we expect to see additional producer insolvencies, which will further reduce activity in the near-term.

Producer cash flows and balance sheets are under pressure, leading to:

Capital spending plans

Debt levels

Availability of credit / capital

Cost to available credit / capital

The Result: E&P’s will maintain spending constraints until cash flow situations improve.

Even in the event we see a significant jump in prices, there remains excess crude held in on and off-shore storage. With over 7,600 drilled-but-uncompleted (DUC) wells and additional wells shut-in, the need for substantial increases in drilling activity will remain low. Overall, our outlook for drilling companies even in a price growth environment (which we expect), is weak for at least the next 12-18 months.

Well service companies may fair marginally better as shut-in wells, and DUC wells come online as these represent a cheaper alternative to adding new production.

As we see production declines in these US basins, we expect to see stability and growth in WTI prices over the next couple of quarters. This may lead to increased capital budgets in 2021, but we believe balance sheets, cash flow and access to capital will remain challenges for many producers into next year.

[1] Monthly additions from one average rig represent EIA’s estimate of an average rig’s contribution to production of oil and natural gas from new wells.