As we welcome a new year, we look at several key trends that are happening in the manufacturing sector. These trends can help companies stay ahead of the curve. The year 2021 has much in store for the manufacturing industry, including four key trends: IoT & AIoT, employee safety, sustainability and 3D printing.

1. IoT & AIoT

IoT & AIoT has been on the rise in the manufacturing industry in recent years and it will continue to be an important aspect in 2021. If you want to learn more about IoT and AIoT, click here. AIoT can include big data, predicative maintenance, industry 4.0 and more. An example of a company inviting in technology and IoT is Siemens. Over the past 10 years, Siemens has spent more than $10 billion acquiring software companies and currently employs more than 24,500 software engineers.

The following Canadian companies are leaders in the IoT sector and can help bring IoT and AIoT to your company.

| Company |

Services |

Website |

|---|---|---|

| Using its AI-CORE™ robotic process automation (RPA) configurable software bots, CoreData can quickly and cost-effectively automate many business and operational processes. | https://www.coredata.ca/ | |

| Utilizing its extensive technical experience in real-time monitoring and control systems for Process Control, Power Utilities, Renewable Energy and Industrial IoT, MR Control Systems have developed a new generation of real-time monitoring and control platform. | http://mrcsi.com/ | |

| TEKTELIC Communications is a recognized supplier of best-in-class LoRaWAN™and NB-IoT Gateways, Sensors and Custom Applications. | https://tektelic.com/ |

A. Big data

Big data is a key aspect of IoT and AIoT in the manufacturing industry. A business capturing big data is able to collect more information than ever before by turning almost any surface into a sensor for data collection. With a greater collection of data, businesses can make more informed decisions to improve efficiency, accuracy and ultimately profitability.

B. Predictive Maintenance

According to ITIC (Information Technology Intelligence Consulting) 98 per cent of manufacturing companies have reported that a single hour of downtime can cost them over $100,000 in lost revenue. Manufacturing companies can use AIoT to leverage real-time operating data to drive improved maintenance planning and execution to increase up time and utilization of assets. Another advantage to predictive maintenance is the ability to schedule maintenance during slower production periods based on the data collected on production trends.

C. Industry 4.0

Industry 4.0 is the enhancement of automation and data exchange technologies in the manufacturing process. This can include adoption of current AI and IoT technology throughout the operations, inside the machinery, in the warehouse and on the workers so that every aspect of an operation can collect data and “talk” to each other. Industry 4.0 can help reduce labour shortages and increase overall efficiency.

Learn more about Industry 4.0 here.

2. Employee safety

Employee safety has always been the top priority for the manufacturing industry, but since the COVID-19 pandemic, safety has become even more critical. 2021 will bring a stronger focus on employee safety and tracking. Many companies may introduce smart protective gear so data from the employees can be collected to help monitor their health and safety.

The sector will be spending more on personal protective equipment (PPE) and sanitization in 2021. In addition to controlling COVID-19, these measures should help increase productivity and employee morale as well as prevent employees from becoming ill and being distracted or worried about their working conditions.

3. Sustainability

For 2021 we believe sustainable manufacturing will continue to be a key trend. There are many benefits to become more sustainable, including reduced costs, increased profit margins and the potential to attract new customers. For more information on the benefits of sustainable manufacturing, click here.

Sustainability for manufacturing also includes localized production and sourcing. Consumers are making it clear that authenticity matters and that they value local products more. Localized production and sourcing also have its benefits such as no tariffs or trade disputes, faster time to market and lower working capital.

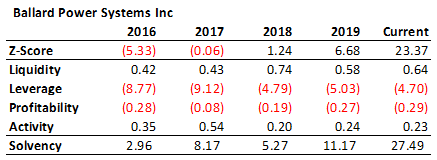

Ballard Power Systems Canada is a great example of a manufacturing company being sustainable. Burnaby based Ballard is a developer and manufacturer of proton exchange membrane fuel cell products for markets such as heavy-duty automotive, portable power, material handling. as well as engineering services. It has manufacturing facilities in Canada and its vision is to help Canada reach a place where there are zero emission fuel cell vehicles. Ballard is dedicated to both improving the environment and localized production.

4. 3D Printing

3D printing has been on the rise for a while. We believe it will continue to be a trend for manufacturing in 2021. In addition to increased affordability, 3D printing is being used to create critical parts, molds, jigs and fixtures for the manufacturing process. In most cases, the custom part can be produced in-house within hours instead of contracted externally with delivery in months. 3D printing also allows companies to make cost effective prototypes that allow product designers to test and troubleshoot new products in a matter of days with significantly reduced waste and lost time.

Conclusion

We believe these four will be the most prominent for many different reasons, including: IoT & AIoT can help companies collect more data leading to better decision making to help save money and increase production. Employee safety will continue to be a priority for companies to keep employees healthy and have higher morale. Sustainability can help reduce costs and make a company more appealing to consumers. Lastly, 3D printing will continue to change the manufacturing industry with the number of different items it can produce in a cost-efficient manner within a short time frame.